How I Built a Smarter Portfolio for a Quality Life—No Luck Needed

What if your investments didn’t just grow—but actually supported the life you want? I used to chase returns blindly, until I realized my portfolio wasn’t backing my lifestyle goals. After a costly mistake, I rebuilt it with clarity: aligning assets with real-life priorities. This isn’t about get-rich-quick schemes. It’s about creating lasting value—through smarter balance, reduced risk, and intentional choices. Here’s how I made my money work meaningfully. For many years, I measured financial success by the numbers on a screen: a rising balance, a trending stock, a friend’s brag about gains. But when the moment came to use that money—booking a family trip, upgrading my home office, or simply taking a break—there was hesitation, fear, even paralysis. My investments were growing, yet I felt poorer in freedom. That disconnect sparked a transformation. I stopped treating my portfolio like a casino scorecard and began seeing it as a structure—like a home—meant to shelter, support, and sustain the life I wanted. This journey wasn’t fueled by luck, genius, or inherited wealth. It was built on deliberate choices, disciplined habits, and a fundamental shift in mindset: that true wealth isn’t how much you have, but how well it serves you.

The Wake-Up Call: When My Portfolio Failed Me

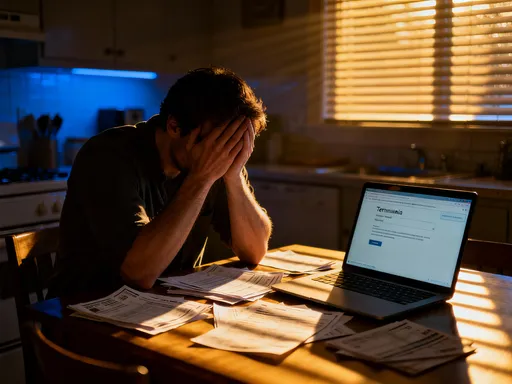

For nearly a decade, my approach to investing was reactive, emotional, and dangerously undisciplined. I followed headlines, bought into trending sectors, and held on during downturns out of hope rather than strategy. My portfolio was a patchwork of speculative stocks, a few mutual funds picked from a list, and a vague belief that time in the market would eventually fix everything. And for a while, it seemed to work—my account balance climbed, and I felt like I was winning. But that win was fragile. When the market dipped sharply during a global economic slowdown, my confidence collapsed faster than my portfolio. I remember sitting at my kitchen table, staring at my phone, watching thousands in paper gains evaporate in a matter of days. I had planned a family vacation to a quiet lakeside retreat—something we hadn’t done in years. But as the red numbers piled up, I canceled the trip, telling my spouse we needed to be ‘responsible.’ The truth was, I was scared. I didn’t know what my investments were truly worth, how long the drop might last, or whether I could afford to spend any of it.

That moment was my wake-up call. I realized I had confused activity with strategy and optimism with planning. My portfolio wasn’t designed to support my life—it was designed to chase performance, with no regard for stability, timing, or personal needs. I had no emergency buffer, no clear asset allocation, and no rules for when to sell or rebalance. Every decision was reactive: buying high out of FOMO, selling low out of fear. I began to ask hard questions: What am I really investing for? When will I need this money? What level of risk can I actually tolerate—not just on paper, but in real life, when the market turns? These questions led me to dismantle my old approach. I sold off speculative holdings, paused new investments temporarily, and committed to building something more thoughtful. I wasn’t starting over with zero knowledge, but with zero excuses. I accepted that past returns didn’t guarantee future security, and that emotional decision-making was the single biggest threat to my financial well-being.

The turning point came when I studied the difference between volatility and risk. Volatility is the normal fluctuation of markets—expected and unavoidable. Risk, however, is the permanent loss of capital or the inability to access funds when needed. I had treated volatility as risk, which led to panic-driven decisions. Once I separated the two, I could design a portfolio that tolerated swings without sacrificing long-term goals. I also recognized that my time horizon mattered more than I thought. For long-term goals like retirement, short-term drops were noise. But for near-term goals like travel or home improvements, those drops were real obstacles. This insight forced me to segment my portfolio by purpose, not just by asset class. It was no longer one monolithic account chasing one vague goal of ‘more money.’ Instead, it became a collection of targeted strategies, each with its own timeline, risk level, and funding mechanism. This structural shift was the foundation of everything that followed.

Redefining Success: Investing for Life, Not Just Gains

Success used to mean outperforming the S&P 500. Now, it means sleeping well at night, having choices, and living without constant financial tension. This redefinition didn’t happen overnight. It emerged from asking a simple but powerful question: What do I want my money to do for me? The answer wasn’t ‘make me rich’—it was ‘give me freedom, security, and the ability to enjoy life without guilt.’ That shift in perspective changed everything. I stopped comparing my returns to others and started measuring progress against my own life goals. I created a personal financial vision board—not with luxury cars or yachts, but with images of family dinners, quiet mornings with coffee, a fully funded education for my children, and the ability to say yes to spontaneous opportunities.

To operationalize this vision, I categorized my financial goals into three timeframes: near-term (0–3 years), mid-term (4–10 years), and long-term (10+ years). Each category demanded a different investment approach. Near-term goals, like vacations or home repairs, required stability and liquidity. I moved these funds into high-yield savings accounts, short-term certificates of deposit, and ultra-short bond funds—vehicles that preserved capital and offered modest but reliable returns. Mid-term goals, such as a future car purchase or a sabbatical, allowed for slightly more growth exposure. I allocated these to balanced funds, dividend-paying stocks, and intermediate bonds—assets that could grow without excessive risk. Long-term goals, primarily retirement, remained in a diversified mix of equities and index funds, where time smoothed out volatility and compounding could work its magic.

This goal-based framework transformed abstract wealth into tangible outcomes. Instead of obsessing over quarterly statements, I tracked progress by asking: Is my lifestyle fund on track? Can I afford the trip next summer? Am I building enough for retirement without overextending? This approach also reduced decision fatigue. I no longer had to guess what to buy or sell each month. My allocations were predetermined, reviewed annually, and adjusted only when life circumstances changed—like a child starting college or a career shift. I also began tracking non-financial metrics: financial stress levels, confidence in decision-making, and the number of ‘no’ moments I could turn into ‘yes.’ These qualitative measures proved just as important as the balance sheet. Wealth, I realized, wasn’t a number—it was a feeling of control, clarity, and readiness for whatever life brought.

The Foundation: Building a Balanced Core Portfolio

My core portfolio is not exciting. It doesn’t make headlines or spark dinner conversation. And that’s exactly why it works. It’s built on the principle that consistency beats heroics. The foundation rests on three pillars: broad market exposure, income stability, and controlled growth. For market exposure, I rely on low-cost, broad-market index funds—primarily total stock market and international index funds. These provide instant diversification across hundreds or thousands of companies, reducing the impact of any single failure. I choose funds with expense ratios below 0.10%, knowing that even small fees compound into massive losses over decades. These holdings make up roughly 50% of my long-term portfolio, serving as the engine of growth over time.

The second pillar is fixed income. I allocate about 30% of my long-term assets to bonds—mostly U.S. Treasury securities, investment-grade municipal bonds, and a small portion of corporate bonds. These aren’t meant to deliver explosive returns; they’re meant to stabilize the portfolio during downturns, provide regular income, and serve as a source of dry powder when equities are cheap. I ladder my bond maturities—spreading them out over several years—so I’m not exposed to interest rate spikes all at once. This structure ensures I always have bonds maturing, giving me flexibility to reinvest or use the cash as needed. For retirees or those nearing retirement, a larger bond allocation may be appropriate, but for my stage—still earning and decades from full retirement—this balance feels right.

The third pillar is selective equity exposure. About 20% of my portfolio is allocated to individual stocks and sector-specific funds, but only after rigorous research. I focus on companies with strong balance sheets, consistent earnings, and sustainable business models—often in healthcare, consumer staples, and utilities. These are not moonshot bets; they’re companies I believe will endure. I limit any single position to no more than 3% of the total portfolio, ensuring no one stock can derail my financial plan. This core structure—index funds, bonds, and select equities—is rebalanced once a year. If one asset class has grown disproportionately, I sell a portion and reinvest in underweight areas. This forces me to ‘buy low and sell high’ systematically, without emotion. The result is a portfolio that doesn’t chase trends but stays aligned with my risk tolerance and long-term goals.

Layering for Lifestyle: Allocating for Quality Living

One of the most liberating changes I made was creating a dedicated lifestyle allocation—5% to 10% of my total portfolio earmarked for experiences and personal enrichment. This isn’t a slush fund or reckless spending. It’s a planned, funded, and protected layer designed to enhance quality of life. I treat it like a separate account with its own rules: it must be fully funded before any withdrawal, it’s invested in income-generating assets, and it’s shielded from the volatility of my core portfolio. The goal is simple: to make meaningful experiences financially sustainable, not one-off indulgences.

I fund this layer through automatic monthly transfers, treating it like any other financial obligation. The money goes into a mix of high-dividend ETFs, real estate investment trusts (REITs), and short-duration bond funds—all chosen for their ability to generate cash flow with moderate risk. Because these assets produce income, I can often cover lifestyle expenses without touching the principal. For example, when I planned a cultural trip to Europe, I didn’t liquidate stocks at a market low. Instead, I used accumulated dividends and interest from this allocation. The trip wasn’t a financial strain—it was a planned outcome of disciplined saving and smart allocation.

This layer also supports ongoing personal growth—things like online courses, wellness programs, or home upgrades that improve daily living. I once invested in a quiet backyard retreat, complete with a small library and meditation space. The initial cost was modest, but the long-term benefit in mental well-being was immense. By funding it through my lifestyle allocation, I avoided dipping into emergency savings or taking on debt. This approach removes guilt from spending on joy. I’m not withdrawing from future security; I’m using a portion of my wealth that was designed for exactly this purpose. It’s a small percentage of my total portfolio, but it delivers disproportionate satisfaction. It reminds me that wealth isn’t just about accumulation—it’s about integration into a life well-lived.

Risk Control: Protecting Gains Without Paralysis

After my early losses, I became obsessed with risk—not as a force to fear, but as a variable to manage. I adopted a barbell strategy, popularized by investors like Nassim Taleb: allocating most of my portfolio to ultra-safe assets while reserving a small portion for higher-risk, higher-potential-return investments. The middle ground—moderately risky assets with uncertain outcomes—I largely avoided. This structure protects the core while allowing for optionality. About 80% of my portfolio is in low-volatility, high-conviction holdings: index funds, Treasuries, and dividend aristocrats. The remaining 20% is split between selective growth stocks, small-cap funds, and occasional thematic investments like clean energy or digital infrastructure.

I also implemented mental stop-loss rules. I don’t use automated sell orders, but I do set price thresholds for review. If a stock drops 15% below my purchase price, I reassess the fundamentals. If the company’s outlook has deteriorated, I sell. If it’s just market noise, I hold or even buy more. This discipline prevents small losses from becoming large ones. I also limit position sizes—no single holding exceeds 3% of the total portfolio—so no one decision can devastate my net worth. Diversification remains my strongest defense. I’m exposed to multiple sectors, geographies, and asset classes, so a downturn in one area doesn’t collapse the whole structure.

Time horizon is another critical risk filter. I never invest money in equities that I’ll need within five years. For those funds, I use cash equivalents or short-term bonds. This prevents me from being forced to sell low during a downturn. I also stress-test my portfolio annually, imagining scenarios like a 30% market drop or a job loss. How would my plan hold up? Do I have enough liquidity? These exercises aren’t meant to induce fear—they’re meant to build confidence through preparation. Over time, I’ve learned that protecting gains is just as important as making them. A 10% return means nothing if the next year brings a 20% loss. Sustainable growth comes from avoiding catastrophic mistakes, not chasing every opportunity.

Practical Moves: Small Adjustments, Big Impact

Some of the most powerful changes I made cost nothing and required no financial genius. They were simple, repeatable habits that compounded over time. The first was automating everything. I set up automatic contributions to my investment accounts, retirement plans, and lifestyle fund. This removed emotion from saving and ensured consistency. Even during tight months, the transfers happened—often in small amounts, but always on time. Over a decade, these automatic deposits added up to tens of thousands in invested capital that I might have otherwise spent or delayed.

The second move was fee reduction. I audited every fund, platform, and service I used. I switched from high-fee mutual funds to low-cost index ETFs, saving an average of 0.75% in annual expenses. On a $100,000 portfolio, that’s $750 per year—$7,500 over ten years, not counting compounding. I also consolidated underperforming accounts, closing outdated IRAs and rolling them into a single, well-managed brokerage. This simplified tracking, reduced fees, and improved tax efficiency. I reviewed advisory fees and, where possible, moved to flat-fee or robo-advisor models that offered better value.

Tax optimization was another quiet game-changer. I maximized contributions to tax-advantaged accounts like 401(k)s and IRAs. I used tax-loss harvesting to offset gains with losses, and I held long-term investments in taxable accounts to benefit from lower capital gains rates. I also timed withdrawals strategically in retirement planning, balancing required minimum distributions with Roth conversions to stay in a lower tax bracket. These moves didn’t make me rich overnight, but they preserved wealth and boosted net returns. Together, automation, fee reduction, and tax efficiency created a foundation of quiet growth—unseen but powerful, like roots beneath a tree.

The Mindset Shift: From Chasing to Building

The most profound change wasn’t in my portfolio—it was in my relationship with money. I stopped seeing investing as a competition and started seeing it as a craft. Patience replaced urgency. Clarity replaced confusion. Intention replaced impulse. I no longer scan headlines for the next hot stock. I don’t check my balance daily. I review my plan quarterly, rebalance annually, and live the rest of the time without financial anxiety. This mindset has improved not just my returns, but my quality of life. I make better decisions because I’m not reacting to noise. I sleep better because I trust my plan. I enjoy life more because I’m not constantly calculating risk.

I’ve also embraced the idea that financial maturity isn’t about having all the answers—it’s about asking the right questions. What am I saving for? How much risk do I really need? Is this decision aligned with my values? These questions keep me grounded. They prevent me from chasing trends or falling for marketing hype. I’ve learned that wealth is not a destination but a process—one that requires ongoing attention, humility, and adjustment. The ultimate return on investment isn’t measured in dollars, but in freedom, peace, and the ability to live with purpose. My portfolio isn’t perfect. Markets will fluctuate. Life will bring surprises. But I now have a structure, a strategy, and a mindset that can handle them. I built a smarter portfolio—not for luck, but for life.